One of the buzz-words in business schools is data analytics or, in an accounting school, accounting analytics. But what exactly is …

Social Media, Organizations, and Academic Research

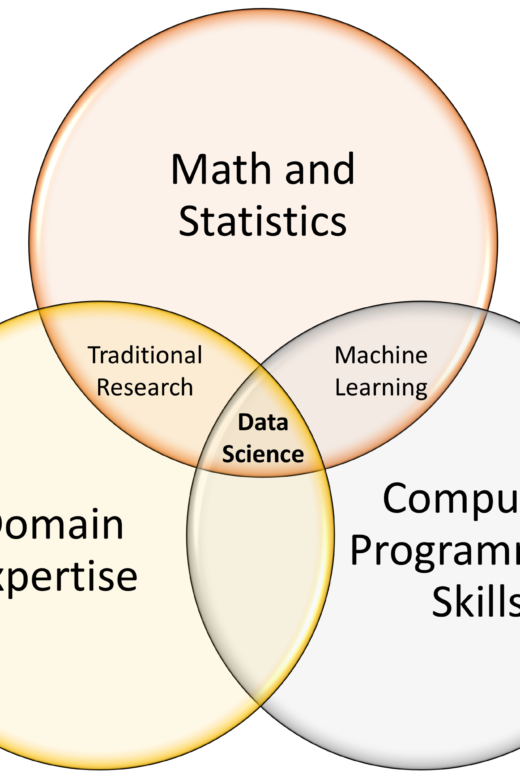

One of the buzz-words in business schools is data analytics or, in an accounting school, accounting analytics. But what exactly is …