This post is Part 3 in my series on intellectual contribution in academic articles. In Part 1 I covered the main types of “contributions” at an abstract level. In Part 2 I turned to the first in a set of posts designed to make the typology concrete by analyzing the type of contribution in the 31 nonprofit-focused articles published to date in The Accounting Review, Journal of Accounting Research, Journal of Accounting & Economics, Contemporary Accounting Research, and Review of Accounting Studies.

The 31 articles are included at the end of this post.

Recap: Four Main Types of Contribution

Before I delve into specifics, let me recap the four central types of contributions:

- Replication

- New Sample or Context

- New Measure (Often with Revised Conceptualization) or New Statistical Technique

- New Relationship

I argued that the first three contributions — replication studies and tests involving new contexts, new definitions, and new measures — are all helpful, but they should not be the sole novelty of any manuscript you’re thinking of sending to a top-tier journal. Instead, by far the most important contribution is testing a new relationship. Why are relationships so important? The short answer: theory. Theory fundamentally involves examining the relationship between two or more concepts. We are making a theoretical argument when we try to explain why one concept (say, earnings management) is determined by another concept (such as pay-for-performance incentives).In effect, when reviewers, discussants, co-authors, or thesis committee chairs are talking about a “contribution” or an “intellectual contribution,” they are almost always referring to a theoretical contribution, which effectively means you are studying one or more new relationships. This means that at a minimum you should strive to add another conceptual relationship to the literature. This could be a new mediator, a new moderator, a new independent variable, or a new dependent variable.

Analyzing the 31 Articles

So, what do I find in the 31 top-tier articles? I find that all 31 test a new relationship. None involve solely a replication, or testing an existing relationship in a new context, or testing an existing relationship with a new measure. In effect, all 31 aim for what I would consider the “gold standard” form of contribution.

Specifically, I found that the typical article examined 1-5 core relationships, not including robustness tests, sensitivity analyses, or additional analyses. Interestingly, few of the studies had core hypotheses with moderating relationships and instead looked at direct X → Y relationships.

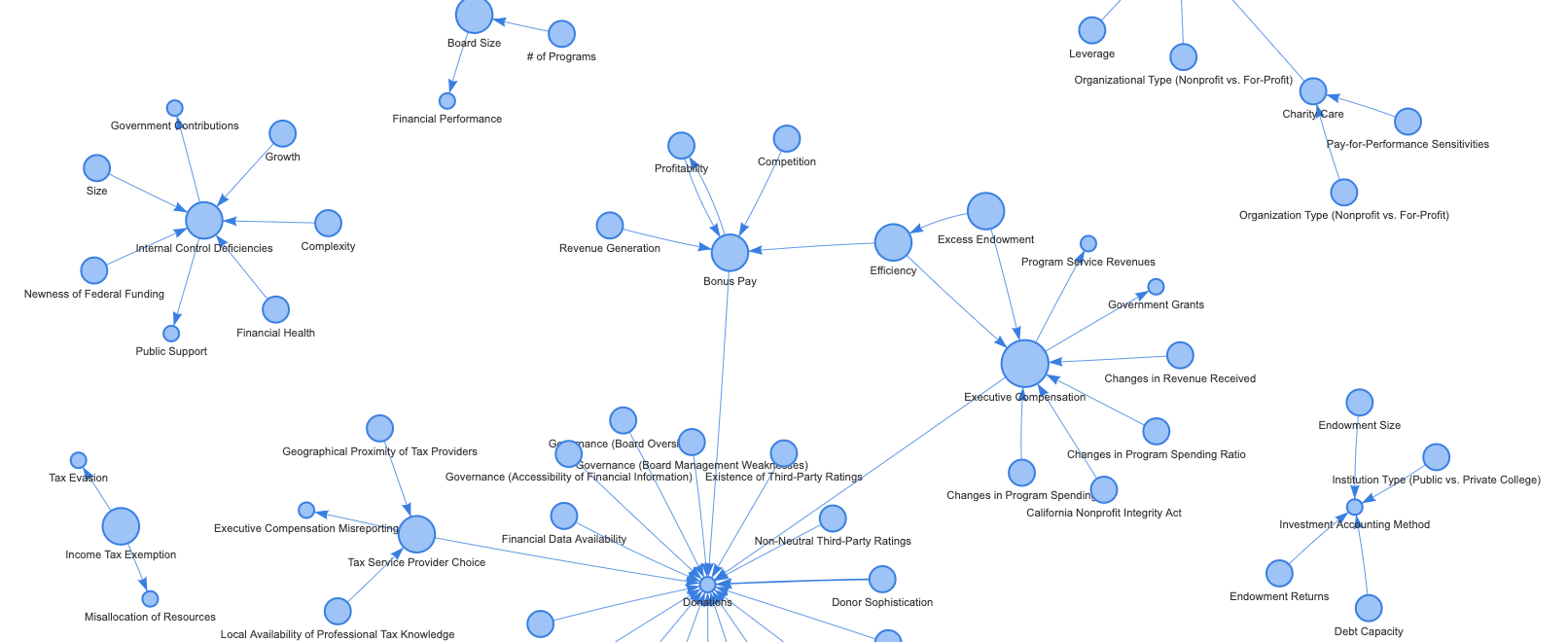

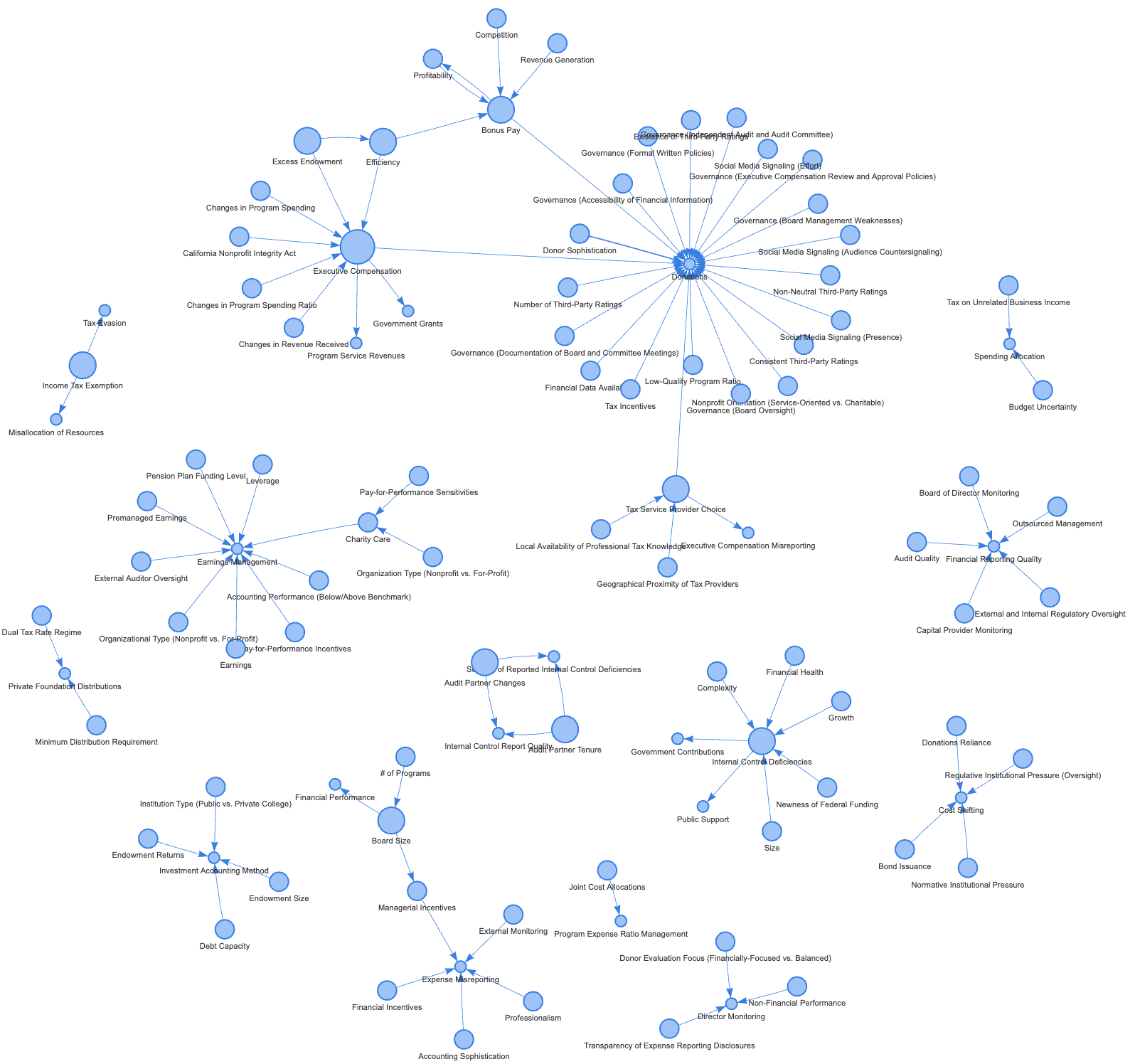

Graphing the Relationships

The figure below maps the relationships found in the 31 articles. Click on the image to see a larger version.

You can see an interactive version of the graph here.

In Part 4 I present the specific relationships examined in each article and show the Networkx code used to generate the network and the above visualization.

List of 31 Articles Published in Top-Tier Accounting Journals

- Harris, E. E., Neely, D. G., & Saxton, G. D. (2021). Social media, signaling, and donations: Testing the financial returns on nonprofits’ social media investment. Review of Accounting Studies, forthcoming. [BibTeX]

@article{Harris2021, Author = {Harris, Erica E and Neely, Daniel G and Saxton, Gregory D}, Date-Added = {2021-09-16 15:33:19 -0400}, Date-Modified = {2021-09-16 15:33:43 -0400}, Journal = {{Review of Accounting Studies}}, Mendeley-Groups = {Top-Tier Nonprofit}, Pages = {forthcoming}, Title = {{Social media, signaling, and donations: Testing the financial returns on nonprofits' social media investment}}, Year = {2021}} -

![[DOI]](https://social-metrics.org/wp-content/plugins/papercite/img/external.png) Finley, A. R., Hall, C. M., & Marino, A. R. (2021). Negotiation and executive gender pay gaps in nonprofit organizations. Review of Accounting Studies. [BibTeX] [Abstract] [PDF]

Finley, A. R., Hall, C. M., & Marino, A. R. (2021). Negotiation and executive gender pay gaps in nonprofit organizations. Review of Accounting Studies. [BibTeX] [Abstract] [PDF]

This study examines gender pay gaps among nonprofit executives and how compensation negotiability influences these disparities. Using tax return data from IRS Form 990 filings, we find that females earn 8.9{\%} lower total compensation than men in our sample. Further, we observe that settings more conducive to negotiation manifest in larger pay disparities, whereas settings that limit executives’ opportunities to negotiate or that encourage females in particular to negotiate produce smaller gender pay gaps. Our nonprofit setting constrains mechanisms, such as labor force participation rates and risk preferences, that are thought to explain the pay gap, and our results are robust to using a Heckman correction model and matched samples. These findings provide evidence from a large-scale archival dataset of a plausible mechanism for the gender pay gap and point to a potential cost of work environments where negotiations play a larger role in setting compensation.

@article{Finley2021, Abstract = {This study examines gender pay gaps among nonprofit executives and how compensation negotiability influences these disparities. Using tax return data from IRS Form 990 filings, we find that females earn 8.9{\%} lower total compensation than men in our sample. Further, we observe that settings more conducive to negotiation manifest in larger pay disparities, whereas settings that limit executives' opportunities to negotiate or that encourage females in particular to negotiate produce smaller gender pay gaps. Our nonprofit setting constrains mechanisms, such as labor force participation rates and risk preferences, that are thought to explain the pay gap, and our results are robust to using a Heckman correction model and matched samples. These findings provide evidence from a large-scale archival dataset of a plausible mechanism for the gender pay gap and point to a potential cost of work environments where negotiations play a larger role in setting compensation.}, Author = {Finley, Andrew R and Hall, Curtis M and Marino, Amanda R}, Date-Added = {2021-09-16 15:33:19 -0400}, Date-Modified = {2021-09-16 15:33:49 -0400}, Doi = {10.1007/s11142-021-09628-2}, Issn = {1573-7136}, Journal = {{Review of Accounting Studies}}, Mendeley-Groups = {Top-Tier Nonprofit}, Title = {{Negotiation and executive gender pay gaps in nonprofit organizations}}, Url = {https://doi.org/10.1007/s11142-021-09628-2}, Year = {2021}, Bdsk-Url-1 = {https://doi.org/10.1007/s11142-021-09628-2}} - Beck, A., Gilstrap, C., Rippy, J., & Vansant, B. (2021). Strategic reporting by nonprofit hospitals: an examination of bad debt and charity care. Review of Accounting Studies. [BibTeX] [Abstract] [PDF]

In this paper, we examine bad debt and charity care reporting by nonprofit hospitals around bond issuance. Given the tax advantages afforded to nonprofit hospitals, including the ability to issue tax-exempt debt, hospital managers encounter stakeholder pressure to provide community benefits. When nonprofits issue debt, they also face economic pressure to meet creditors’ financial performance expectations. We document a reporting strategy that allows nonprofit hospitals to reduce the cost of bond debt while simultaneously alleviating regulators’ and community members’ concerns about inadequate provision of charity care. Using data from public bond issues for California nonprofit hospitals, we find that hospital managers shift costs from bad debt expense to charity care in periods prior to a public bond issuance and that the strategy is associated with a lower cost of debt. Our results inform those relying on accounting measurements to infer nonprofit hospitals’ social good provisions and financial health.

@article{Beck2021, Abstract = {In this paper, we examine bad debt and charity care reporting by nonprofit hospitals around bond issuance. Given the tax advantages afforded to nonprofit hospitals, including the ability to issue tax-exempt debt, hospital managers encounter stakeholder pressure to provide community benefits. When nonprofits issue debt, they also face economic pressure to meet creditors' financial performance expectations. We document a reporting strategy that allows nonprofit hospitals to reduce the cost of bond debt while simultaneously alleviating regulators' and community members' concerns about inadequate provision of charity care. Using data from public bond issues for California nonprofit hospitals, we find that hospital managers shift costs from bad debt expense to charity care in periods prior to a public bond issuance and that the strategy is associated with a lower cost of debt. Our results inform those relying on accounting measurements to infer nonprofit hospitals' social good provisions and financial health.}, Author = {Beck, Amanda and Gilstrap, Collin and Rippy, Jordan and Vansant, Brian}, Date-Added = {2021-09-16 15:33:19 -0400}, Date-Modified = {2021-09-16 15:33:58 -0400}, Doi = {10.1007/s11142-021-09624-6}, Issn = {1573-7136}, Journal = {{Review of Accounting Studies}}, Mendeley-Groups = {ACTG 7020,Top-Tier Nonprofit}, Title = {{Strategic reporting by nonprofit hospitals: an examination of bad debt and charity care}}, Url = {https://doi.org/10.1007/s11142-021-09624-6}, Year = {2021}, Bdsk-Url-1 = {https://doi.org/10.1007/s11142-021-09624-6}} - Balsam, S., & Harris, E. E. (2018). Nonprofit executive incentive pay. Review of Accounting Studies, 23(4), 1665–1714. [BibTeX] [Abstract] [PDF]

We utilize information only recently disclosed on Form 990 to examine the use, and consequences of, incentive pay at nonprofit organizations. Bonuses are common in nonprofits, as we observe that approximately 45{\%} of the 44,000 organization-year observations in our sample reported paying CEO bonuses. We find that the bonuses are positively associated with profitability, competition from other nonprofits, firm size, available cash, and use of compensation consultants and committees, while negatively related to board oversight, donations, and grants. Our results also suggest that donors look unfavorably at the payment of bonuses; that is, bonuses are associated with lower future donations. Nonetheless, we find evidence consistent with the payment of bonuses incentivizing nonprofit executives, as despite reduced fundraising, future profitability and program services are positively associated with current bonus compensation.

@article{Balsam2018, Abstract = {We utilize information only recently disclosed on Form 990 to examine the use, and consequences of, incentive pay at nonprofit organizations. Bonuses are common in nonprofits, as we observe that approximately 45{\%} of the 44,000 organization-year observations in our sample reported paying CEO bonuses. We find that the bonuses are positively associated with profitability, competition from other nonprofits, firm size, available cash, and use of compensation consultants and committees, while negatively related to board oversight, donations, and grants. Our results also suggest that donors look unfavorably at the payment of bonuses; that is, bonuses are associated with lower future donations. Nonetheless, we find evidence consistent with the payment of bonuses incentivizing nonprofit executives, as despite reduced fundraising, future profitability and program services are positively associated with current bonus compensation.}, Author = {Balsam, Steven and Harris, Erica E}, Date-Added = {2020-11-10 12:05:21 -0500}, Date-Modified = {2020-11-10 12:05:30 -0500}, Doi = {10.1007/s11142-018-9473-z}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/Nonprofit executive incentive pay.pdf:pdf}, Issn = {1573-7136}, Journal = {{Review of Accounting Studies}}, Number = {4}, Pages = {1665--1714}, Title = {{Nonprofit executive incentive pay}}, Url = {https://doi.org/10.1007/s11142-018-9473-z}, Volume = {23}, Year = {2018}, Bdsk-Url-1 = {https://doi.org/10.1007/s11142-018-9473-z}} - Fitzgerald, B. C., Omer, T. C., & Thompson, A. M. (2018). Audit partner tenure and internal control reporting quality: U.S. evidence from the not‐for‐profit sector. Contemporary Accounting Research, 35(1), 334–364. [BibTeX] [Abstract]

Abstract This study examines the effects of audit partner tenure and audit partner changes on internal control reporting quality for large U.S. not‐for‐profit (NFP) organizations. Regulators contend that audit partners lose their objectivity over successive audits, reducing audit quality. A large body of research has examined this issue, primarily in non‐U.S. jurisdictions, with mixed results. We examine the associations between audit partner tenure and audit partner changes and the incidence of reported internal control deficiencies (ICDs), the quality of internal control reports (following PCAOB audit quality indicators), and the severity of reported ICDs. We find negative associations between audit partner tenure and the incidence of reported ICDs, the quality of internal control reports, and the severity of reported ICDs. Together, these findings indicate that internal control reporting quality deteriorates with audit partner tenure. However, we find no association between audit partner changes and internal control reporting, which is consistent with partners lacking client specific knowledge in their first year with a client. Finally, we find no association between either audit partner tenure or changes and the likelihood of remediation. Our findings contribute large‐sample U.S. evidence on the association between audit partner tenure and internal control reporting quality and provide useful information to government regulators, NFP boards charged with the oversight of the external auditor and internal controls, and NFP stakeholders.

@article{Fitzgerald2018, Abstract = {Abstract This study examines the effects of audit partner tenure and audit partner changes on internal control reporting quality for large U.S. not‐for‐profit (NFP) organizations. Regulators contend that audit partners lose their objectivity over successive audits, reducing audit quality. A large body of research has examined this issue, primarily in non‐U.S. jurisdictions, with mixed results. We examine the associations between audit partner tenure and audit partner changes and the incidence of reported internal control deficiencies (ICDs), the quality of internal control reports (following PCAOB audit quality indicators), and the severity of reported ICDs. We find negative associations between audit partner tenure and the incidence of reported ICDs, the quality of internal control reports, and the severity of reported ICDs. Together, these findings indicate that internal control reporting quality deteriorates with audit partner tenure. However, we find no association between audit partner changes and internal control reporting, which is consistent with partners lacking client specific knowledge in their first year with a client. Finally, we find no association between either audit partner tenure or changes and the likelihood of remediation. Our findings contribute large‐sample U.S. evidence on the association between audit partner tenure and internal control reporting quality and provide useful information to government regulators, NFP boards charged with the oversight of the external auditor and internal controls, and NFP stakeholders.}, Author = {Fitzgerald, Brian C and Omer, Thomas C and Thompson, Anne M}, Date-Modified = {2018-04-26 23:59:08 +0000}, Doi = {10.1111/1911-3846.12348}, Issn = {0823-9150}, Journal = {Contemporary {A}ccounting {R}esearch}, Number = {1}, Pages = {334--364}, Title = {{Audit partner tenure and internal control reporting quality: U.S. evidence from the not‐for‐profit sector}}, Volume = {35}, Year = {2018}, Bdsk-Url-1 = {http://resolver.scholarsportal.info/resolve/08239150/v35i0001/334%7B%5C_%7Daptaicueftns}, Bdsk-Url-2 = {http://dx.doi.org/10.1111/1911-3846.12348}} - Chen, Q. (2016). Director monitoring of expense misreporting in nonprofit organizations: The effects of expense disclosure transparency, donor evaluation focus and organization performance. Contemporary Accounting Research, 33(4), 1601–1624. [BibTeX] [Abstract]

Abstract This study examines whether three factors–-the transparency of expense disclosures, donor evaluation focus, and organization performance–-influence how directors monitor management expense misreporting in nonprofit organizations. An experiment with 189 nonprofit directors finds that the enhanced transparency of expense disclosures increases director monitoring by reducing the tendency to accept management expense misreporting. Further, an organization’s nonfinancial performance and the perceived fairness of donor evaluation focus interact to influence director monitoring practices. Specifically, when directors know an organization’s nonfinancial performance is poor and understand that this performance will negatively influence the willingness of donors to contribute, directors monitor less if they think that donors are adopting a more balanced approach to organizational evaluation that focuses on both financial and nonfinancial performance; that is, there is a reverse fair process effect as this donor approach is perceived as being fairer than if donors focus solely on financial performance. However, monitoring is equally strong regardless of donor evaluation focus when directors know that an organization’s nonfinancial performance is good and a donation is forthcoming.

@article{Chen2016, Abstract = {Abstract This study examines whether three factors---the transparency of expense disclosures, donor evaluation focus, and organization performance---influence how directors monitor management expense misreporting in nonprofit organizations. An experiment with 189 nonprofit directors finds that the enhanced transparency of expense disclosures increases director monitoring by reducing the tendency to accept management expense misreporting. Further, an organization's nonfinancial performance and the perceived fairness of donor evaluation focus interact to influence director monitoring practices. Specifically, when directors know an organization's nonfinancial performance is poor and understand that this performance will negatively influence the willingness of donors to contribute, directors monitor less if they think that donors are adopting a more balanced approach to organizational evaluation that focuses on both financial and nonfinancial performance; that is, there is a reverse fair process effect as this donor approach is perceived as being fairer than if donors focus solely on financial performance. However, monitoring is equally strong regardless of donor evaluation focus when directors know that an organization's nonfinancial performance is good and a donation is forthcoming.}, Author = {Chen, Qiu}, Date-Modified = {2018-04-27 00:00:38 +0000}, Doi = {10.1111/1911-3846.12218}, Issn = {0823-9150}, Journal = {Contemporary {A}ccounting {R}esearch}, Number = {4}, Pages = {1601--1624}, Publisher = {Wiley}, Title = {{Director monitoring of expense misreporting in nonprofit organizations: The effects of expense disclosure transparency, donor evaluation focus and organization performance}}, Volume = {33}, Year = {2016}, Bdsk-Url-1 = {http://resolver.scholarsportal.info/resolve/08239150/v33i0004/1601%7B%5C_%7Ddmoemidefaop}, Bdsk-Url-2 = {http://dx.doi.org/10.1111/1911-3846.12218}} - Vansant, B. (2016). Institutional pressures to provide social benefits and the earnings management behavior of nonprofits: Evidence from the U.S. hospital industry. Contemporary Accounting Research, 33(4), 1576–1600. [BibTeX] [Abstract]

Abstract This study examines the relationship between institutional pressures to provide social benefits and the discretionary accrual behavior of nonprofit firms. I examine this issue within the context of U.S. nonprofit hospitals, an economically significant and politically rich setting where firms face considerable institutional pressure to provide an important social benefit: charity care. I argue that institutional pressures on nonprofits to provide higher levels of social benefits imply that lower profits should be reported. I develop theory and provide evidence which suggests that, due to competing private incentives to report higher profits, nonprofit managers strategically use discretionary accruals to increase accounting earnings when the social benefits their firms have provided in the current period exceed external stakeholders’ normative expectations. The findings from this study inform the ongoing political debate regarding the appropriateness of tax exemptions for U.S. nonprofit hospitals and should therefore be of interest to both regulators and policymakers. In addition, this study provides timely insights for researchers regarding how institutional pressures can affect managers’ reporting behaviors in other settings where similar competing reporting incentives exist between managers’ private benefits and stakeholder expectations related to social benefits.

@article{Vansant2016, Abstract = {Abstract This study examines the relationship between institutional pressures to provide social benefits and the discretionary accrual behavior of nonprofit firms. I examine this issue within the context of U.S. nonprofit hospitals, an economically significant and politically rich setting where firms face considerable institutional pressure to provide an important social benefit: charity care. I argue that institutional pressures on nonprofits to provide higher levels of social benefits imply that lower profits should be reported. I develop theory and provide evidence which suggests that, due to competing private incentives to report higher profits, nonprofit managers strategically use discretionary accruals to increase accounting earnings when the social benefits their firms have provided in the current period exceed external stakeholders' normative expectations. The findings from this study inform the ongoing political debate regarding the appropriateness of tax exemptions for U.S. nonprofit hospitals and should therefore be of interest to both regulators and policymakers. In addition, this study provides timely insights for researchers regarding how institutional pressures can affect managers' reporting behaviors in other settings where similar competing reporting incentives exist between managers' private benefits and stakeholder expectations related to social benefits.}, Author = {Vansant, Brian}, Date-Modified = {2018-04-26 23:59:14 +0000}, Doi = {10.1111/1911-3846.12215}, Issn = {0823-9150}, Journal = {Contemporary {A}ccounting {R}esearch}, Number = {4}, Pages = {1576--1600}, Publisher = {Wiley}, Title = {{Institutional pressures to provide social benefits and the earnings management behavior of nonprofits: Evidence from the U.S. hospital industry}}, Volume = {33}, Year = {2016}, Bdsk-Url-1 = {http://resolver.scholarsportal.info/resolve/08239150/v33i0004/1576%7B%5C_%7Diptpsbnetuhi}, Bdsk-Url-2 = {http://dx.doi.org/10.1111/1911-3846.12215}} - Harris, E. E., & Neely, D. G. (2015). Multiple information signals in the market for charitable donations. Contemporary Accounting Research, 33(3), 989–1012. [BibTeX] [Abstract]

Abstract We find evidence indicating that donors use third?party rating information when they donate to U.S. nonprofit organizations (nonprofits). Specifically, using a sample of over 3,800 unique nonprofits rated by the three largest charity rating organizations in 2007, and over 12,000 unrated control nonprofits, we find that rated nonprofits have significantly higher direct donations than unrated charities. We also hypothesize and find that nonprofits with ratings from multiple rating organizations receive incrementally higher levels of donations. In addition, although charities that receive a positive rating have higher levels of donor support than those receiving a negative rating, both positively and negatively rated nonprofits receive a higher level of direct donations than unrated nonprofits. Finally, we find that nonprofits with consistently good ratings receive higher donations than those with mixed or consistently negative ratings, indicating the donor community values consistency across the three rating agencies.

@article{E.2015, Abstract = {Abstract We find evidence indicating that donors use third?party rating information when they donate to U.S. nonprofit organizations (nonprofits). Specifically, using a sample of over 3,800 unique nonprofits rated by the three largest charity rating organizations in 2007, and over 12,000 unrated control nonprofits, we find that rated nonprofits have significantly higher direct donations than unrated charities. We also hypothesize and find that nonprofits with ratings from multiple rating organizations receive incrementally higher levels of donations. In addition, although charities that receive a positive rating have higher levels of donor support than those receiving a negative rating, both positively and negatively rated nonprofits receive a higher level of direct donations than unrated nonprofits. Finally, we find that nonprofits with consistently good ratings receive higher donations than those with mixed or consistently negative ratings, indicating the donor community values consistency across the three rating agencies.}, Annote = {doi: 10.1111/1911-3846.12175}, Author = {Erica E. Harris and Daniel G. Neely}, Date-Modified = {2018-04-27 00:03:15 +0000}, Doi = {10.1111/1911-3846.12175}, Issn = {0823-9150}, Journal = {Contemporary {A}ccounting {R}esearch}, Month = {oct}, Number = {3}, Pages = {989--1012}, Publisher = {Wiley/Blackwell (10.1111)}, Title = {{Multiple information signals in the market for charitable donations}}, Volume = {33}, Year = {2015}, Bdsk-Url-1 = {https://doi.org/10.1111/1911-3846.12175}, Bdsk-Url-2 = {http://dx.doi.org/10.1111/1911-3846.12175}} - Neuman, S. S., Omer, T. C., & Thompson, A. M. (2015). Determinants and consequences of tax service provider choice in the not‐for‐profit sector. Contemporary Accounting Research, 32(2), 703–735. [BibTeX]

@article{Neuman2015, Author = {Neuman, Stevanie S and Omer, Thomas C and Thompson, Anne M}, Date-Modified = {2018-04-26 23:59:19 +0000}, Doi = {10.1111/1911-3846.12080}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/Determinants and Consequences of Tax Service Provider Choice in the Not‐for‐Profit Sector.pdf:pdf}, Issn = {0823-9150}, Journal = {Contemporary {A}ccounting {R}esearch}, Number = {2}, Pages = {703--735}, Publisher = {Wiley}, Title = {{Determinants and consequences of tax service provider choice in the not‐for‐profit sector}}, Volume = {32}, Year = {2015}, Bdsk-Url-1 = {http://resolver.scholarsportal.info/resolve/08239150/v32i0002/703%7B%5C_%7Ddacotspcitns}, Bdsk-Url-2 = {http://dx.doi.org/10.1111/1911-3846.12080}} - Eldenburg, L. G., Gaertner, F. B., & Goodman, T. H. (2015). The influence of ownership and compensation practices on charitable activities. Contemporary Accounting Research, 32(1), 169–192. [BibTeX] [Abstract]

Abstract Recent accounting research provides evidence that similar profit‐based compensation incentives are used in for‐profit and nonprofit hospitals. Because charity care reduces profits, such incentives should lead for‐profit hospital managers to reduce charity care levels. Nonprofit hospital managers, however, may respond differently to the same incentives because they face a different set of institutional pressures and constraints. We compare the association between pay‐for‐performance incentives and charity care in for‐profit and nonprofit hospitals. We find a negative and significant association between charity care and our proxy for profit‐based incentives in for‐profit hospitals, and no significant association in nonprofit hospitals. These results suggest that linking manager pay to profitability does not appear to discourage charity care in nonprofit hospitals. Apparently, the nonprofit mission, institutional pressures, and ownership constraints moderate the potentially negative effects of profit‐based incentives. Because this evidence partially alleviates concerns over nonprofit compensation arrangements that mirror those used in for‐profit hospitals, it should be of interest to regulators and policymakers. In addition, this study provides insights into accounting researchers about institutional and organizational influences that affect managerial responses to financial incentives in compensation contracts.

@article{Eldenburg2015, Abstract = {Abstract Recent accounting research provides evidence that similar profit‐based compensation incentives are used in for‐profit and nonprofit hospitals. Because charity care reduces profits, such incentives should lead for‐profit hospital managers to reduce charity care levels. Nonprofit hospital managers, however, may respond differently to the same incentives because they face a different set of institutional pressures and constraints. We compare the association between pay‐for‐performance incentives and charity care in for‐profit and nonprofit hospitals. We find a negative and significant association between charity care and our proxy for profit‐based incentives in for‐profit hospitals, and no significant association in nonprofit hospitals. These results suggest that linking manager pay to profitability does not appear to discourage charity care in nonprofit hospitals. Apparently, the nonprofit mission, institutional pressures, and ownership constraints moderate the potentially negative effects of profit‐based incentives. Because this evidence partially alleviates concerns over nonprofit compensation arrangements that mirror those used in for‐profit hospitals, it should be of interest to regulators and policymakers. In addition, this study provides insights into accounting researchers about institutional and organizational influences that affect managerial responses to financial incentives in compensation contracts.}, Author = {Eldenburg, Leslie G and Gaertner, Fabio B and Goodman, Theodore H}, Date-Modified = {2018-04-27 00:00:27 +0000}, Doi = {10.1111/1911-3846.12066}, Issn = {0823-9150}, Journal = {Contemporary {A}ccounting {R}esearch}, Number = {1}, Pages = {169--192}, Publisher = {Wiley}, Title = {{The influence of ownership and compensation practices on charitable activities}}, Volume = {32}, Year = {2015}, Bdsk-Url-1 = {http://resolver.scholarsportal.info/resolve/08239150/v32i0001/169%7B%5C_%7Dtiooacpoca}, Bdsk-Url-2 = {http://dx.doi.org/10.1111/1911-3846.12066}} - Dhole, S., Khumawala, S. B., Mishra, S., & Ranasinghe, T. (2014). Executive compensation and regulation-imposed governance: Evidence from the California Nonprofit Integrity Act of 2004. The Accounting Review, 90(2), 443–466. [BibTeX] [PDF]

@article{Dhole2014, Annote = {doi: 10.2308/accr-50942}, Author = {Dhole, Sandip and Khumawala, Saleha B and Mishra, Sagarika and Ranasinghe, Tharindra}, Date-Modified = {2018-04-27 00:04:41 +0000}, Doi = {10.2308/accr-50942}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/Executive Compensation and Regulation-Imposed Governance - Evidence from the California Nonprofit Integrity Act of 2004.pdf:pdf}, Issn = {0001-4826}, Journal = {The {A}ccounting {R}eview}, Month = {oct}, Number = {2}, Pages = {443--466}, Publisher = {American Accounting Association}, Title = {{Executive compensation and regulation-imposed governance: Evidence from the California Nonprofit Integrity Act of 2004}}, Url = {https://doi.org/10.2308/accr-50942}, Volume = {90}, Year = {2014}, Bdsk-Url-1 = {https://doi.org/10.2308/accr-50942}, Bdsk-Url-2 = {http://dx.doi.org/10.2308/accr-50942}} - Harris, E., Petrovits, C. M., & Yetman, M. H. (2014). The effect of nonprofit governance on donations: Evidence from the revised Form 990. The Accounting Review, 90(2), 579–610. [BibTeX] [PDF]

@article{Harris2014a, Annote = {doi: 10.2308/accr-50874}, Author = {Harris, Erica and Petrovits, Christine M and Yetman, Michelle H}, Date-Modified = {2018-04-27 00:04:46 +0000}, Doi = {10.2308/accr-50874}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/The Effect of Nonprofit Governance on Donations - Evidence from the Revised Form 990.pdf:pdf}, Issn = {0001-4826}, Journal = {The {A}ccounting {R}eview}, Month = {jul}, Number = {2}, Pages = {579--610}, Publisher = {American Accounting Association}, Title = {{The effect of nonprofit governance on donations: Evidence from the revised Form 990}}, Url = {https://doi.org/10.2308/accr-50874}, Volume = {90}, Year = {2014}, Bdsk-Url-1 = {https://doi.org/10.2308/accr-50874}, Bdsk-Url-2 = {http://dx.doi.org/10.2308/accr-50874}} - Vermeer, T. E., Edmonds, C. T., & Asthana, S. C. (2014). Organizational form and accounting choice: Are nonprofit or for-profit managers more aggressive?. The Accounting Review, 89(5), 1867–1893. [BibTeX] [PDF]

@article{Vermeer2014, Annote = {doi: 10.2308/accr-50796}, Author = {Vermeer, Thomas E and Edmonds, Christopher T and Asthana, Sharad C}, Date-Modified = {2018-04-27 00:04:53 +0000}, Doi = {10.2308/accr-50796}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/Organizational Form and Accounting Choice - Are Nonprofit or For-Profit Managers More Aggressive.pdf:pdf}, Issn = {0001-4826}, Journal = {The {A}ccounting {R}eview}, Month = {apr}, Number = {5}, Pages = {1867--1893}, Publisher = {American Accounting Association}, Title = {{Organizational form and accounting choice: Are nonprofit or for-profit managers more aggressive?}}, Url = {https://doi.org/10.2308/accr-50796}, Volume = {89}, Year = {2014}, Bdsk-Url-1 = {https://doi.org/10.2308/accr-50796}, Bdsk-Url-2 = {http://dx.doi.org/10.2308/accr-50796}} - Balsam, S., & Harris, E. E. (2013). The impact of CEO compensation on nonprofit donations. The Accounting Review, 89(2), 425–450. [BibTeX] [PDF]

@article{Balsam2013, Annote = {doi: 10.2308/accr-50631}, Author = {Balsam, Steven and Harris, Erica E}, Date-Modified = {2018-04-27 00:05:13 +0000}, Doi = {10.2308/accr-50631}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/The Impact of CEO Compensation on Nonprofit Donations.pdf:pdf}, Issn = {0001-4826}, Journal = {The {A}ccounting {R}eview}, Month = {oct}, Number = {2}, Pages = {425--450}, Publisher = {American Accounting Association}, Title = {{The impact of CEO compensation on nonprofit donations}}, Url = {https://doi.org/10.2308/accr-50631}, Volume = {89}, Year = {2013}, Bdsk-Url-1 = {https://doi.org/10.2308/accr-50631}, Bdsk-Url-2 = {http://dx.doi.org/10.2308/accr-50631}} - Yetman, M. H., & Yetman, R. J. (2012). Do donors discount low-quality accounting information?. The Accounting Review, 88(3), 1041–1067. [BibTeX] [PDF]

@article{Yetman2012b, Annote = {doi: 10.2308/accr-50367}, Author = {Yetman, Michelle H and Yetman, Robert J}, Date-Modified = {2018-04-26 23:57:31 +0000}, Doi = {10.2308/accr-50367}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/Do Donors Discount Low-Quality Accounting Information.pdf:pdf}, Issn = {0001-4826}, Journal = {The {A}ccounting {R}eview}, Month = {dec}, Number = {3}, Pages = {1041--1067}, Publisher = {American Accounting Association}, Title = {{Do donors discount low-quality accounting information?}}, Url = {https://doi.org/10.2308/accr-50367}, Volume = {88}, Year = {2012}, Bdsk-Url-1 = {https://doi.org/10.2308/accr-50367}, Bdsk-Url-2 = {http://dx.doi.org/10.2308/accr-50367}} - Yetman, M. H., & Yetman, R. J. (2012). How does the incentive effect of the charitable deduction vary across charities?. The Accounting Review, 88(3), 1069–1094. [BibTeX] [PDF]

@article{Yetman2012c, Annote = {doi: 10.2308/accr-50370}, Author = {Yetman, Michelle H and Yetman, Robert J}, Date-Modified = {2018-04-26 23:57:24 +0000}, Doi = {10.2308/accr-50370}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/How Does the Incentive Effect of the Charitable Deduction Vary across Charities.pdf:pdf}, Issn = {0001-4826}, Journal = {The {A}ccounting {R}eview}, Month = {dec}, Number = {3}, Pages = {1069--1094}, Publisher = {American Accounting Association}, Title = {{How does the incentive effect of the charitable deduction vary across charities?}}, Url = {https://doi.org/10.2308/accr-50370}, Volume = {88}, Year = {2012}, Bdsk-Url-1 = {https://doi.org/10.2308/accr-50370}, Bdsk-Url-2 = {http://dx.doi.org/10.2308/accr-50370}} - H., Y. M., & J., Y. R. (2012). The effects of governance on the accuracy of charitable expenses reported by nonprofit organizations. Contemporary Accounting Research, 29(3), 738–767. [BibTeX]

@article{H.2012, Annote = {doi: 10.1111/j.1911-3846.2011.01121.x}, Author = {H., Yetman Michelle and J., Yetman Robert}, Date-Modified = {2018-04-26 23:59:28 +0000}, Doi = {10.1111/j.1911-3846.2011.01121.x}, Issn = {0823-9150}, Journal = {Contemporary {A}ccounting {R}esearch}, Month = {sep}, Number = {3}, Pages = {738--767}, Publisher = {Wiley/Blackwell (10.1111)}, Title = {{The effects of governance on the accuracy of charitable expenses reported by nonprofit organizations}}, Volume = {29}, Year = {2012}, Bdsk-Url-1 = {https://doi.org/10.1111/j.1911-3846.2011.01121.x}, Bdsk-Url-2 = {http://dx.doi.org/10.1111/j.1911-3846.2011.01121.x}} - Aggarwal, R. K., Evans, M. E., & Nanda, D. (2012). Nonprofit boards: Size, performance and managerial incentives. Journal of Accounting and Economics, 53(1-2), 466–487. [BibTeX] [Abstract] [PDF]

Abstract We examine relations between board size, managerial incentives and enterprise performance in nonprofit organizations. We posit that a nonprofit’s demand for directors increases in the number of programs it pursues, resulting in a positive association between program diversity and board size. Consequently, we predict that board size is inversely related to managerial pay-performance incentives and positively with overall organization performance. We find empirical evidence consistent with our hypotheses. The number of programs is positively related to board size. Board size is associated negatively with managerial incentives, positively with program spending and fundraising performance, and negatively with commercial revenue, in levels and changes.

@article{Aggarwal2012a, Abstract = {Abstract We examine relations between board size, managerial incentives and enterprise performance in nonprofit organizations. We posit that a nonprofit's demand for directors increases in the number of programs it pursues, resulting in a positive association between program diversity and board size. Consequently, we predict that board size is inversely related to managerial pay-performance incentives and positively with overall organization performance. We find empirical evidence consistent with our hypotheses. The number of programs is positively related to board size. Board size is associated negatively with managerial incentives, positively with program spending and fundraising performance, and negatively with commercial revenue, in levels and changes.}, Author = {Aggarwal, Rajesh K and Evans, Mark E and Nanda, Dhananjay}, Date-Modified = {2018-04-26 23:56:49 +0000}, Doi = {10.1016/j.jacceco.2011.08.001}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/Nonprofit boards - Size, performance and managerial incentives.pdf:pdf}, Issn = {01654101}, Journal = {Journal of {A}ccounting and {E}conomics}, Keywords = {Boards of directors,D21,G34,Incentives,J33,L31,M40,Nonprofits}, Number = {1-2}, Pages = {466--487}, Publisher = {Elsevier}, Title = {{Nonprofit boards: Size, performance and managerial incentives}}, Url = {http://resolver.scholarsportal.info/resolve/01654101/v53i1-2/466{\_}nbspami}, Volume = {53}, Year = {2012}, Bdsk-Url-1 = {http://resolver.scholarsportal.info/resolve/01654101/v53i1-2/466%7B%5C_%7Dnbspami}, Bdsk-Url-2 = {http://dx.doi.org/10.1016/j.jacceco.2011.08.001}} - Eldenburg, L. G., Gunny, K. A., Hee, K. W., & Soderstrom, N. (2011). Earnings management using real activities: Evidence from nonprofit hospitals. The Accounting Review, 86(5), 1605–1630. [BibTeX] [PDF]

@article{Eldenburg2011, Annote = {doi: 10.2308/accr-10095}, Author = {Eldenburg, Leslie G and Gunny, Katherine A and Hee, Kevin W and Soderstrom, Naomi}, Date-Modified = {2018-04-27 00:05:25 +0000}, Doi = {10.2308/accr-10095}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/Earnings Management Using Real Activities - Evidence from Nonprofit Hospitals.pdf:pdf}, Issn = {0001-4826}, Journal = {The {A}ccounting {R}eview}, Month = {may}, Number = {5}, Pages = {1605--1630}, Publisher = {American Accounting Association}, Title = {{Earnings management using real activities: Evidence from nonprofit hospitals}}, Url = {https://doi.org/10.2308/accr-10095}, Volume = {86}, Year = {2011}, Bdsk-Url-1 = {https://doi.org/10.2308/accr-10095}, Bdsk-Url-2 = {http://dx.doi.org/10.2308/accr-10095}} - Krishnan, R., & Yetman, M. H. (2011). Institutional drivers of reporting decisions in nonprofit hospitals. Journal of Accounting Research, 49(4), 1001–1039. [BibTeX] [Abstract]

ABSTRACT We examine the influence of normative and regulative institutional factors on cost shifting by nonprofit hospitals in their publicly reported statements. We explore whether normative constraints imposed by stakeholders, who prefer that nonprofit hospitals allocate their resources toward patient‐related program services, influence the extent to which nonprofit hospitals shift costs toward program services and away from administrative and fundraising categories, thereby appearing more efficient. We also explore whether regulative factors, such as oversight, influence cost shifting behaviors. Results indicate that nonprofit hospitals facing higher normative pressures to demonstrate efficiency shift costs to a greater extent, and hospitals facing higher regulatory oversight shift costs to a lesser extent. Consistent with prior research, we also find that hospitals that obtain higher donations revenue shift costs to a greater extent. Our results show that, in addition to economic factors documented by prior literature, institutional factors also influence nonprofit hospitals’ cost shifting behaviors.

@article{KRISHNAN2011, Abstract = {ABSTRACT We examine the influence of normative and regulative institutional factors on cost shifting by nonprofit hospitals in their publicly reported statements. We explore whether normative constraints imposed by stakeholders, who prefer that nonprofit hospitals allocate their resources toward patient‐related program services, influence the extent to which nonprofit hospitals shift costs toward program services and away from administrative and fundraising categories, thereby appearing more efficient. We also explore whether regulative factors, such as oversight, influence cost shifting behaviors. Results indicate that nonprofit hospitals facing higher normative pressures to demonstrate efficiency shift costs to a greater extent, and hospitals facing higher regulatory oversight shift costs to a lesser extent. Consistent with prior research, we also find that hospitals that obtain higher donations revenue shift costs to a greater extent. Our results show that, in addition to economic factors documented by prior literature, institutional factors also influence nonprofit hospitals' cost shifting behaviors.}, Author = {Krishnan, Ranjani and Yetman, Michelle H}, Date-Modified = {2018-04-27 00:00:53 +0000}, Doi = {10.1111/j.1475-679X.2011.00413.x}, Issn = {0021-8456}, Journal = {Journal of {A}ccounting {R}esearch}, Number = {4}, Pages = {1001--1039}, Publisher = {Blackwell Publishing Inc}, Title = {{Institutional drivers of reporting decisions in nonprofit hospitals}}, Volume = {49}, Year = {2011}, Bdsk-Url-1 = {http://resolver.scholarsportal.info/resolve/00218456/v49i0004/1001%7B%5C_%7Didordinh}, Bdsk-Url-2 = {http://dx.doi.org/10.1111/j.1475-679X.2011.00413.x}} - Petrovits, C., Shakespeare, C., & Shih, A. (2011). The causes and consequences of internal control problems in nonprofit organizations. The Accounting Review, 86(1), 325–357. [BibTeX] [Abstract]

This study examines the causes and consequences of internal control deficiencies in the nonprofit sector using a sample of 27,495 public charities from 1999 to 2007. We first document that the likelihood of reporting an internal control problem increases for nonprofit organizations that are in poor financial health, growing, more complex, and/or smaller. We then present evidence that the disclosure of weak internal controls over financial reporting is negatively associated with subsequent donor support received after controlling for the current level of donor support and other factors influ- encing donations. We likewise report a negative association between internal control problems and subsequent government grants. Our results suggest that donors and government agencies, important sources of capital for nonprofit organizations, react either directly or indirectly to internal control information.

@article{petrovits2011causes, Abstract = {This study examines the causes and consequences of internal control deficiencies in the nonprofit sector using a sample of 27,495 public charities from 1999 to 2007. We first document that the likelihood of reporting an internal control problem increases for nonprofit organizations that are in poor financial health, growing, more complex, and/or smaller. We then present evidence that the disclosure of weak internal controls over financial reporting is negatively associated with subsequent donor support received after controlling for the current level of donor support and other factors influ- encing donations. We likewise report a negative association between internal control problems and subsequent government grants. Our results suggest that donors and government agencies, important sources of capital for nonprofit organizations, react either directly or indirectly to internal control information.}, Author = {Petrovits, Christine and Shakespeare, Catherine and Shih, Aimee}, Date-Modified = {2018-04-27 00:05:31 +0000}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/The Causes and Consequences of Internal Control Problems in Nonprofit Organizations.pdf:pdf}, Journal = {The {A}ccounting {R}eview}, Number = {1}, Pages = {325--357}, Title = {{The causes and consequences of internal control problems in nonprofit organizations}}, Volume = {86}, Year = {2011}} - Keating, E. K., Parsons, L. M., & Roberts, A. A. (2008). Misreporting fundraising: How do nonprofit organizations account for telemarketing campaigns?. The Accounting Review, 83(2), 417–446. [BibTeX] [Abstract]

The purpose of this study is to examine the frequency, determinants, and implications of misreported fundraising activities. We compare state telemarketing campaign reports with the associated information from nonprofits’ annual Form 990 filings to directly test nonprofits’ revenue and expense recognition policies. Using a conservative approach that understates the extent to which nonprofit organizations violate the reporting rules, our study indicates that 74 percent of the regulatory filings from nonprofit organizations fail to properly report telemarketing expenses. Smaller nonprofits, less monitored firms, and those with less accounting sophistication are more likely to inappropriately report telemarketing costs as a component of net revenues rather than as expenses. Nonprofits that use external accounting services are more likely to properly classify the cost of their telemarketing campaigns as professional fundraising fees.

@article{Keating2008, Abstract = {The purpose of this study is to examine the frequency, determinants, and implications of misreported fundraising activities. We compare state telemarketing campaign reports with the associated information from nonprofits' annual Form 990 filings to directly test nonprofits' revenue and expense recognition policies. Using a conservative approach that understates the extent to which nonprofit organizations violate the reporting rules, our study indicates that 74 percent of the regulatory filings from nonprofit organizations fail to properly report telemarketing expenses. Smaller nonprofits, less monitored firms, and those with less accounting sophistication are more likely to inappropriately report telemarketing costs as a component of net revenues rather than as expenses. Nonprofits that use external accounting services are more likely to properly classify the cost of their telemarketing campaigns as professional fundraising fees.}, Author = {Keating, Elizabeth K and Parsons, Linda M and Roberts, Andrea Alston}, Date-Modified = {2018-04-27 00:05:35 +0000}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/Misreporting Fundraising - How Do Nonprofit Organizations Account for Telemarketing Campaigns.pdf:pdf}, Issn = {0001-4826}, Journal = {The {A}ccounting {R}eview}, Number = {2}, Pages = {417--446}, Title = {{Misreporting fundraising: How do nonprofit organizations account for telemarketing campaigns?}}, Volume = {83}, Year = {2008}} - Jones, C. L., & Roberts, A. A. (2006). Management of financial information in charitable organizations: The case of joint‐cost allocations. The Accounting Review, 81(1), 159–178. [BibTeX] [PDF]

@article{Jones2006a, Annote = {doi: 10.2308/accr.2006.81.1.159}, Author = {Jones, Christopher L and Roberts, Andrea Alston}, Date-Modified = {2018-04-27 00:05:43 +0000}, Doi = {10.2308/accr.2006.81.1.159}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/Management of Financial Information in Charitable Organizations - The Case of Joint‐Cost Allocations.pdf:pdf}, Issn = {0001-4826}, Journal = {The {A}ccounting {R}eview}, Month = {jan}, Number = {1}, Pages = {159--178}, Publisher = {American Accounting Association}, Title = {{Management of financial information in charitable organizations: The case of joint‐cost allocations}}, Url = {https://doi.org/10.2308/accr.2006.81.1.159}, Volume = {81}, Year = {2006}, Bdsk-Url-1 = {https://doi.org/10.2308/accr.2006.81.1.159}, Bdsk-Url-2 = {http://dx.doi.org/10.2308/accr.2006.81.1.159}} - Sansing, R., & Yetman, R. (2006). Governing private foundations using the tax law. Journal of Accounting and Economics, 41(3), 363–384. [BibTeX] [Abstract] [PDF]

This paper investigates two tax law provisions that act as governance instruments designed to regulate the behavior of private foundations. It examines tax return data from a sample of private foundations to determine the effects of the minimum distribution requirement and the dual tax rate regime. The minimum distribution requirement primarily affects the distribution behavior of foundations that are no longer receiving donations and are growing more slowly than the average foundation. The dual tax rate regime has countervailing effects on distributions by foundations, rewarding both higher levels of current distributions and lower levels of prior year distributions.

@article{Sansing2006, Abstract = {This paper investigates two tax law provisions that act as governance instruments designed to regulate the behavior of private foundations. It examines tax return data from a sample of private foundations to determine the effects of the minimum distribution requirement and the dual tax rate regime. The minimum distribution requirement primarily affects the distribution behavior of foundations that are no longer receiving donations and are growing more slowly than the average foundation. The dual tax rate regime has countervailing effects on distributions by foundations, rewarding both higher levels of current distributions and lower levels of prior year distributions.}, Author = {Sansing, Richard and Yetman, Robert}, Date-Added = {2020-11-10 12:07:19 -0500}, Date-Modified = {2020-11-10 12:07:28 -0500}, Doi = {https://doi.org/10.1016/j.jacceco.2005.03.003}, Issn = {0165-4101}, Journal = {Journal of {A}ccounting and {E}conomics}, Keywords = {Governance,Non-profit organizations,Philanthropy,Private foundations}, Number = {3}, Pages = {363--384}, Title = {{Governing private foundations using the tax law}}, Url = {http://www.sciencedirect.com/science/article/pii/S0165410105000650}, Volume = {41}, Year = {2006}, Bdsk-Url-1 = {http://www.sciencedirect.com/science/article/pii/S0165410105000650}, Bdsk-Url-2 = {https://doi.org/10.1016/j.jacceco.2005.03.003}} - Core, J. E., Guay, W. R., & Verdi, R. S. (2006). Agency problems of excess endowment holdings in not-for-profit firms. Journal of Accounting and Economics, 41(3), 307–333. [BibTeX] [Abstract] [PDF]

We examine three alternative explanations for excess endowments in not-for-profit firms: (1) growth opportunities, (2) monitoring, or (3) agency problems. Inconsistent with growth opportunities, we find that most excess endowments are persistent over time, and that firms with persistent excess endowments do not exhibit higher growth in program expenses or investments. Inconsistent with better monitoring, program expenditures toward the charitable good are lower for firms with excess endowments, and CEO pay and total officer and director pay are greater for firms with excess endowments. Overall, we find that excess endowments are associated with greater agency problems.

@article{Core2006, Abstract = {We examine three alternative explanations for excess endowments in not-for-profit firms: (1) growth opportunities, (2) monitoring, or (3) agency problems. Inconsistent with growth opportunities, we find that most excess endowments are persistent over time, and that firms with persistent excess endowments do not exhibit higher growth in program expenses or investments. Inconsistent with better monitoring, program expenditures toward the charitable good are lower for firms with excess endowments, and CEO pay and total officer and director pay are greater for firms with excess endowments. Overall, we find that excess endowments are associated with greater agency problems.}, Author = {Core, J E and Guay, W R and Verdi, R S}, Date-Modified = {2018-04-26 23:56:37 +0000}, Doi = {10.1016/j.jacceco.2006.02.001}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/Agency problems of excess endowment holdings in not-for-profit firms.pdf:pdf}, Issn = {0165-4101}, Journal = {Journal of {A}ccounting and {E}conomics}, Keywords = {Agency problems,Cash holdings,Corporate governance,Endowment,Not-for-profit,[jel] G31,[jel] G35,[jel] G38,[jel] J33,[jel] L31}, Number = {3}, Pages = {307--333}, Publisher = {Elsevier Science}, Title = {{Agency problems of excess endowment holdings in not-for-profit firms}}, Url = {http://resolver.scholarsportal.info/resolve/01654101/v41i0003/307{\_}apoeehinf}, Volume = {41}, Year = {2006}, Bdsk-Url-1 = {http://resolver.scholarsportal.info/resolve/01654101/v41i0003/307%7B%5C_%7Dapoeehinf}, Bdsk-Url-2 = {http://dx.doi.org/10.1016/j.jacceco.2006.02.001}} - Bolton, P., & Mehran, H. (2006). An introduction to the governance and taxation of not-for-profit organizations. Journal of Accounting and Economics, 41(3), 293–305. [BibTeX] [Abstract] [PDF]

This paper provides a brief overview of the current state of the not-for-profit sector and discusses specific governance issues in not-for-profit organizations. We offer an in-depth analysis of the issues that arise when not-for-profit organizations compete against for-profit firms in the same markets. We argue that while competition by for-profit firms can discipline not-for-profit firms and mitigate their governance problems, the effects of this competition are distorted by the not-for-profits’ corporate income tax exemptions. Based on a simple general equilibrium analysis, we argue that there is little justification for such exemptions.

@article{Bolton2006, Abstract = {This paper provides a brief overview of the current state of the not-for-profit sector and discusses specific governance issues in not-for-profit organizations. We offer an in-depth analysis of the issues that arise when not-for-profit organizations compete against for-profit firms in the same markets. We argue that while competition by for-profit firms can discipline not-for-profit firms and mitigate their governance problems, the effects of this competition are distorted by the not-for-profits' corporate income tax exemptions. Based on a simple general equilibrium analysis, we argue that there is little justification for such exemptions.}, Author = {Bolton, P and Mehran, H}, Date-Modified = {2018-04-26 23:56:45 +0000}, Doi = {10.1016/j.jacceco.2006.06.001}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/An introduction to the governance and taxation of not-for-profit organizations.pdf:pdf}, Issn = {0165-4101}, Journal = {Journal of {A}ccounting and {E}conomics}, Keywords = {Governance,Not-for-profit,Taxation,[jel] G18,[jel] G3,[jel] H2}, Number = {3}, Pages = {293--305}, Publisher = {Elsevier Science}, Title = {{An introduction to the governance and taxation of not-for-profit organizations}}, Url = {http://resolver.scholarsportal.info/resolve/01654101/v41i0003/293{\_}aittgatono}, Volume = {41}, Year = {2006}, Bdsk-Url-1 = {http://resolver.scholarsportal.info/resolve/01654101/v41i0003/293%7B%5C_%7Daittgatono}, Bdsk-Url-2 = {http://dx.doi.org/10.1016/j.jacceco.2006.06.001}} - Krishnan R., Yetman M.H., & Yetman, R. J. (2006). Expense misreporting in nonprofit organizations. The Accounting Review, 81, 399–420. [BibTeX] [Abstract]

We examine whether nonprofit organizations understate fundraising expenses in their publicly available financial statements. A large body of anecdotal evidence notes that an inexplicable number of nonprofits report zero fundraising expenses. We provide empirical evidence that the zero fundraising expense phenomenon is at least partly due to inappropriate reporting. We then examine to what extent these misreported expenses are the result of managerial incentives. Prior research finds an association between reported expenses and managerial compensation as well as the level of donations received. Using these findings we construct two incentive variables and find a positive association between misreporting behavior and managerial incentives. Our results also suggest that the use of an outside accountant reduces the probability that a nonprofit will misreport expenses, consistent with the use of an outside paid accountant increasing the reliability and usefulness of nonprofit financial reports. Finally, we find that SOP 98‐2 reduced the probability that a nonprofit will misreport fundraising expenses.

@article{Krishnan2006, Abstract = {We examine whether nonprofit organizations understate fundraising expenses in their publicly available financial statements. A large body of anecdotal evidence notes that an inexplicable number of nonprofits report zero fundraising expenses. We provide empirical evidence that the zero fundraising expense phenomenon is at least partly due to inappropriate reporting. We then examine to what extent these misreported expenses are the result of managerial incentives. Prior research finds an association between reported expenses and managerial compensation as well as the level of donations received. Using these findings we construct two incentive variables and find a positive association between misreporting behavior and managerial incentives. Our results also suggest that the use of an outside accountant reduces the probability that a nonprofit will misreport expenses, consistent with the use of an outside paid accountant increasing the reliability and usefulness of nonprofit financial reports. Finally, we find that SOP 98‐2 reduced the probability that a nonprofit will misreport fundraising expenses.}, Author = {{Krishnan R.} and {Yetman M.H.} and Yetman, R J}, Date-Modified = {2018-04-27 00:05:47 +0000}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/Expense Misreporting in Nonprofit Organizations.pdf:pdf}, Journal = {The {A}ccounting {R}eview}, Pages = {399--420}, Title = {{Expense misreporting in nonprofit organizations}}, Volume = {81}, Year = {2006}} - Baber, W. R., Daniel, P. L., & Roberts, A. A. (2002). Compensation to managers of charitable organizations: An empirical study of the role of accounting measures of program activities. The Accounting Review, 77(3), 679–693. [BibTeX] [PDF]

@article{Baber2002, Author = {Baber, William R and Daniel, Patricia L and Roberts, Andrea A}, Date-Modified = {2018-04-27 00:05:52 +0000}, Doi = {10.2308/accr.2002.77.3.679}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/Compensation to Managers of Charitable Organizations - An Empirical Study of the Role of Accounting Measures of Program Activities.pdf:pdf}, Journal = {The {A}ccounting {R}eview}, Number = {3}, Pages = {679--693}, Publisher = {AAA}, Title = {{Compensation to managers of charitable organizations: An empirical study of the role of accounting measures of program activities}}, Url = {http://link.aip.org/link/?TAR/77/679/1}, Volume = {77}, Year = {2002}, Bdsk-Url-1 = {http://link.aip.org/link/?TAR/77/679/1}, Bdsk-Url-2 = {http://dx.doi.org/10.2308/accr.2002.77.3.679}} - Yetman, R. J. (2001). Tax‐motivated expense allocations by nonprofit organizations. The Accounting Review, 76(3), 297–311. [BibTeX] [PDF]

@article{Yetman2001, Annote = {doi: 10.2308/accr.2001.76.3.297}, Author = {Yetman, Robert J}, Date-Modified = {2018-04-27 00:05:56 +0000}, Doi = {10.2308/accr.2001.76.3.297}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/Tax‐Motivated Expense Allocations by Nonprofit Organizations.pdf:pdf}, Issn = {0001-4826}, Journal = {The {A}ccounting {R}eview}, Month = {jul}, Number = {3}, Pages = {297--311}, Publisher = {American Accounting Association}, Title = {{Tax‐motivated expense allocations by nonprofit organizations}}, Url = {https://doi.org/10.2308/accr.2001.76.3.297}, Volume = {76}, Year = {2001}, Bdsk-Url-1 = {https://doi.org/10.2308/accr.2001.76.3.297}, Bdsk-Url-2 = {http://dx.doi.org/10.2308/accr.2001.76.3.297}} - Chase, B. W., & Coffman, E. N. (1994). Choice of accounting method by not-for-profit institutions accounting for investments by colleges and universities. Journal of Accounting and Economics, 18(2), 233–243. [BibTeX] [Abstract] [PDF]

This study reports a preliminary empirical investigation into the relation between the choice of investment accounting method used by colleges and universities and factors such as type of institution, endowment size and returns, and debt. Because these institutions use fund accounting, the effects of the choice of investment accounting method can reasonably be isolated from other accounting decisions. The results indicate that the selection of investment accounting method is influenced by type of institution, endowment size and returns, but not by debt covenants.

@article{Chase1994, Abstract = {This study reports a preliminary empirical investigation into the relation between the choice of investment accounting method used by colleges and universities and factors such as type of institution, endowment size and returns, and debt. Because these institutions use fund accounting, the effects of the choice of investment accounting method can reasonably be isolated from other accounting decisions. The results indicate that the selection of investment accounting method is influenced by type of institution, endowment size and returns, but not by debt covenants.}, Author = {Chase, Bruce W and Coffman, Edward N}, Date-Modified = {2018-04-26 23:56:41 +0000}, Doi = {10.1016/0165-4101(94)00360-2}, File = {:Users/gsaxton/Dropbox/Mendeley PDFs/Choice of accounting method by not-for-profit institutions accounting for investments by colleges and universities.pdf:pdf}, Issn = {0165-4101}, Journal = {Journal of {A}ccounting and {E}conomics}, Keywords = {Accounting choice,M4,Not-for-profit political process}, Number = {2}, Pages = {233--243}, Publisher = {Elsevier Science}, Title = {{Choice of accounting method by not-for-profit institutions accounting for investments by colleges and universities}}, Url = {http://resolver.scholarsportal.info/resolve/01654101/v18i0002/233{\_}coambnfibcau}, Volume = {18}, Year = {1994}, Bdsk-Url-1 = {http://resolver.scholarsportal.info/resolve/01654101/v18i0002/233%7B%5C_%7Dcoambnfibcau}, Bdsk-Url-2 = {http://dx.doi.org/10.1016/0165-4101(94)00360-2}} - Zimmerman, J. L. (1976). Budget uncertainty and the allocation decision in a nonprofit organization. Journal of Accounting Research, 14(2), 301–319. [BibTeX]

@article{Zimmerman1976, Author = {Zimmerman, Jerold L}, Date-Modified = {2018-04-27 00:00:47 +0000}, Doi = {10.2307/2490545}, Issn = {00218456}, Journal = {Journal of {A}ccounting {R}esearch}, Number = {2}, Pages = {301--319}, Publisher = {Accounting Research Center, Booth School of Business, University of Chicago;Blackwell Publishing}, Title = {{Budget uncertainty and the allocation decision in a nonprofit organization}}, Volume = {14}, Year = {1976}, Bdsk-Url-1 = {http://resolver.scholarsportal.info/resolve/00218456/v14i0002/301%7B%5C_%7Dbuatadiano}, Bdsk-Url-2 = {http://dx.doi.org/10.2307/2490545}}